Getting a loan for a house owner isn’t an easy task. There is so much paperwork and time taking process. But here, we have a solution that works really fast and the complete process is online. If you have enough equity in your house then you can take a loan from the penfed up to $500,000.

Here, is our complete penfed heloc review post where we have covered everything about the penfed credit union HELOC.

A brief overview of PenFed home equity loan

As a flexible lending option, PenFed, or Pentagon Federal Credit Union, provides home equity loans to its members. With a home equity loan, you can take out a loan against the equity in your home, which is the sum of the outstanding mortgage balance and the home’s value. Depending on your situation, you may be able to deduct the interest paid on the loan from your taxes and use the loan funds for whatever purpose. Members can submit applications online or at PenFed, which offers competitive interest rates.

Must read- Universal Credit Loan- Best Personal Loan Up To $50,000

How Does PenFed home equity loan Work?

Using the equity in your house as collateral for a loan is possible with a PenFed home equity loan. The loan has a lower interest rate than an unsecured loan because it is secured by your house. This is how it goes:

Analyze your home’s equity to see how much you own there: You must own your house with at least 20% equity in order to be eligible for a PenFed home equity loan. Subtract your mortgage debt from the market value of your home to determine your equity.

You can apply for a PenFed Home Equity Loan online or in person at one of their branches. You’ll have to present supporting evidence, such as a copy of your mortgage statement and proof of income.

Accept the loan offer: If you accept the loan’s terms, you must sign a loan agreement and give PenFed any further paperwork that may be needed.

After your loan has been accepted and is complete, PenFed will send you the money in one lump amount. You are free to utilize the funds however you see fit.

You must repay the loan in full, including interest and principal, each month. The normal loan period is up to 20 years, with a fixed interest rate throughout with 8.125% APR.

The loan will be ended after PenFed releases the lien on your house as a result of your full repayment of the loan.

It’s crucial to remember that you run the risk of losing your property to foreclosure if you don’t make your loan payments on time. Before applying, it’s crucial to thoroughly assess if a home equity loan is the best option for your financial position.

The Benefits of a PenFed Home Equity Loan

For homeowners who have equity built up in their houses, a PenFed home equity loan provided by the Pentagon Federal Credit Union can offer a number of advantages. Here are a few potential advantages:

Access to Cash: A home equity loan enables you to draw funds from your home’s equity, which is the difference between the property’s fair market value and the outstanding mortgage sum. The upshot of this is that you can obtain money without having to list your house or get a personal loan.

Reduced Interest Rates: Since home equity loans are backed by your house rather than unsecured loans like credit cards or personal loans, they often have lower interest rates.

Fixed Payments: Throughout the duration of your PenFed home equity loan, your monthly payment will be fixed at a certain amount. Making a budget and planning for your monthly costs may become simpler as a result.

Possible tax advantages: You may be able to deduct the interest you pay on a home equity loan, which can lower your overall tax burden. Yet, it’s crucial to speak with a tax expert to ascertain whether you qualify for this deduction.

Flexible Repayment Terms: PenFed offers home equity loans with flexible repayment durations ranging from 5 to 20 years. You can select the repayment period that best suits your financial condition.

In general, homeowners who need access to cash and have equity in their houses may find a PenFed home equity loan to be a suitable choice. Before applying, it’s crucial to carefully review the conditions and costs of the loan.

Must read- Best Discover Home Equity Loan Reviews -Is it Right for you?

How Much Equity Can You Borrow with a PenFed Home Equity Loan?

Your property’s current market value, the amount still owed on your mortgage, and PenFed’s loan-to-value (LTV) ratio criteria will all affect how much equity you are eligible to borrow with a PenFed home equity loan.

You can typically borrow up to 90% of the equity in your house with PenFed, though the exact amount may change depending on your credit rating, income, and other criteria. Start by determining your home’s current market worth, then deduct the total owed on your mortgage to determine the maximum amount you can borrow. Your available equity, for instance, would be $20,000 if your house is worth $500,000 and you owe $300,000 on your mortgage.

Your available equity would then be multiplied by PenFed’s 90% maximum LTV ratio. The most you could borrow in this scenario would be $180,000.

It’s crucial to keep in mind that not everyone should borrow the maximum allowed because doing so may result in higher monthly payments and, in the event of nonpayment, a possible risk to your house. To choose the right borrowing amount for your requirements, it’s crucial to thoroughly analyze your financial status and consult a PenFed representative.

Factors that determine the amount of equity you can borrow against

The amount of a PenFed home equity loan might vary depending on a number of variables. They consist of:

Home Equity: A key consideration in determining the size of a PenFed home equity loan is how much equity you have in your home. The equity in your house is the sum of the current market value minus the remaining mortgage balance. You could be able to borrow more money if your equity is higher.

Credit Score: Your credit score plays a significant role in determining how much money you can borrow. Generally speaking, a higher credit score results in a smaller interest rate and a greater loan amount.

Income and Employment: While calculating the amount of your loan, PenFed will also take into account your income and employment history.

Loan-to-Value Ratio (LTV): Your mortgage balance is compared to the worth of your home to determine your LTV ratio. You can borrow up to 90% of the value of your property with a PenFed home equity loan because PenFed normally has a maximum LTV requirement of 90%.

Property Type: Your loan amount may vary depending on the type of property you possess. For principal houses, second homes, and investment properties, PenFed may have varying criteria.

Your debt-to-income ratio (DTI) measures how much debt you have in relation to your income. A maximum DTI of 50% is normally required by PenFed, which means that your total loan payments cannot be greater than 50% of your income. Your ability to borrow more money may increase if your DTI ratio decreases.

How to calculate the maximum loan amount

You must take a number of things into account when determining the maximum loan amount for a PenFed home equity loan. The procedures you can take to determine your maximum loan amount are summarised in the following broad outline:

Finding the current market value of your home might be the first step in determining its worth. You may assess the worth of your house using a number of online resources. A more precise estimate can be obtained by hiring an appraiser as an alternative.

Determine your home equity: The next step is to determine your home equity by deducting the outstanding mortgage balance from the current market value of your home.

Examine the loan-to-value (LTV) ratio: For a home equity loan, PenFed normally requires a maximum LTV of 90%. The valuation of your home multiplied by 0.9 (90%), will give you the maximum loan amount you are permitted to take out.

Take into account your DTI ratio and credit score: Your maximum loan amount eligibility may also be impacted by your credit score and DTI ratio. You might be able to borrow more money than someone with a lower credit score and a higher DTI ratio if you have a high credit score and a low DTI ratio.

Contact a PenFed agent: Contacting a PenFed representative is the best approach to finding out your maximum loan amount. They can assess your financial condition and provide you with an estimation of the maximum loan you qualify for.

It’s crucial to keep in mind that these are only basic recommendations and that each borrower’s circumstances may vary. The maximum loan amount can also be affected by variables like income, employment history, and property type. To fully grasp your possibilities and choose the ideal loan amount for your requirements, it is always recommended to consult with a knowledgeable lender.

Must read- Upstart Loan Reviews : Is it Best choice for Loans?

What Can You Use a PenFed Home Equity Loan For?

There are several uses for a PenFed home equity loan, including:

Home improvements: You can utilize a home equity loan to make upgrades to your house, such as putting in new flooring, adding a room, or remodeling the kitchen.

Debt consolidation: You can use a home equity loan to combine high-interest debt, such as credit card debt or personal loans, into a single payment each month at a lower interest rate.

Education costs: You are able to use a home equity loan to pay for educational costs like tuition, books, or other supplies.

Medical expenses such as unanticipated medical bills, surgeries, or treatments, may be covered by a home equity loan.

Large purchases: A home equity loan might give you the money you need to finance a major purchase, such as a car or a boat.

Dream vacations and travel arrangements can be paid for with a home equity loan.

Home equity loans can be used to pay for company expenses like buying goods, and equipment, or expanding your operations.

Although a home equity loan might give you access to money for a variety of things, it’s crucial to use the money sensibly and within your limits. For further information about the potential advantages and disadvantages of using a home equity loan for your particular requirements, you should also consult a skilled financial advisor.

The Benefits of PenFed Home Equity Loan

A PenFed home equity loan has a number of advantages, including:

Access to Funds: A home equity loan can give you access to a sizeable sum of money for a number of things, such as debt consolidation, home upgrades, medical bills, education costs, major purchases, and more.

Reduced Interest Rates: As compared to other loan kinds, including credit cards or personal loans, home equity loans often have lower interest rates. In the long term, this can help you save money, particularly if you’re consolidating high-interest debt.

Predictable Payments: A home equity loan’s fixed interest rate and monthly payments make it simpler to organize your finances and create a budget. Knowing that your prices will continue to be steady might be reassuring.

Possible tax advantages: A home equity loan’s interest payment may occasionally qualify for a tax deduction. To determine whether you qualify for any potential tax savings, it’s crucial to speak with a skilled tax practitioner.

Flexibility: You can choose to withdraw the entire amount at once or in smaller amounts over time with a home equity loan, giving you freedom in how you spend the money.

PenFed does not impose prepayment penalties on home equity loans, so you are free to pay off your loan early without incurring additional costs.

Reduced Closing Costs: Compared to other lenders, PenFed may provide cheaper closing charges, which can help you save money upfront.

All things considered, a PenFed home equity loan can give you access to money at a reduced interest rate with regular payments, potential tax advantages, and no prepayment fees. To decide whether a home equity loan is the best financial choice for your particular circumstances, it’s critical to examine the potential advantages and disadvantages of taking one out.

Eligibility for a PenFed Home Equity Loan

Depending on your individual financial circumstances and the loan type you’re looking for, the requirements for a PenFed home equity loan may change. Nonetheless, PenFed might take into account the following general eligibility criteria:

Penfed heloc credit score requirements: To be eligible for a PenFed Home Equity Loan, you must have acceptable credit. You must have a score of 680 or above to maximize your chances of approval.

Home equity: To be eligible for a home equity loan, your home must have enough equity. PenFed normally has a maximum loan-to-value (LTV) ratio of 90%, which means that the sum of your current mortgage balance and the amount you intend to borrow cannot be greater than 90% of the worth of your house as determined by the appraiser.

DTI (debt-to-income) ratio: Your DTI ratio is the proportion of your gross monthly income to your monthly debt payments. Your chances of being approved for a home equity loan may rise if your DTI ratio is lower because it often denotes greater financial stability.

Employment and income: You must have a history of a steady job and have enough money coming in each month to make loan payments. You must provide proof of your income with 1 – 2 months of paychecks and at least 2 months of your most recent bank account statements.

Property type: The kinds of properties that are eligible for a home equity loan may be subject to limits by PenFed. For instance, certain properties, such as co-ops or investment properties, could not be eligible.

Additional considerations: When considering your eligibility for a home equity loan, PenFed may take into account additional considerations, such as your 2-years of tax returns, credit utilization, and other debts like auto, alimony, credit card, etc.

It’s crucial to remember that fulfilling these eligibility criteria does not ensure approval for a PenFed home equity loan. The purpose of the loan, the size of the loan, and your general financial health are all things that lenders could take into account when reviewing your application.

Fee charged on home equity loan penfed

There are some cares on penfed HELOC when you apply for a new home equity loan. Here, in the table below you, can see the charges for different activities on penfed-

| Fees For | Total fee |

|---|---|

| Convenience Check Stop Payment (Individual) | $20 |

| Annual HELOC Fee | $99 |

| Over Credit Limit | $20 |

| Lien Release Processing | $20 |

| Late Charge | On the basis of the promissory note |

| Returned Check | $30 |

How to Apply for a PenFed Home Equity Loan

By doing the following, you can apply for a PenFed home equity loan:

Find out if you’re qualified: Be sure you satisfy PenFed’s qualifying requirements before submitting an application for a home equity loan. To find out more, check out the PenFed website’s eligibility requirements or get in touch with a representative.

Assemble your papers: To support your loan application, you’ll need to submit specific papers, such as your mortgage statement, proof of income, and homeowner’s insurance information. Before you start the application process, make sure you have all the required documentation.

Apply online or in person at a PenFed branch to submit an application for a PenFed Home Equity Loan. The entire application procedure lasts about 15 minutes. Visit penfed website. here, click on the MORTGAGE & HOME EQUITY menu. Then clicks on the get started button. It will ask you to choose the type of loan you want and click on the home equity loan and provide all the supported tins.

Await approval: After you complete your application, PenFed will evaluate your credit history and financial data to decide whether you qualify for a home equity loan. During the underwriting process, you can be asked for more information or documentation.

Close on your loan: If your application for a home equity loan is accepted, you’ll get a loan estimate and closing disclosure that contains information about the loan’s terms and conditions. Before the loan can be funded, you must read over and sign these papers.

Utilize the money: After your home equity loan has been funded, you can put the money to whatever use you have in mind, such as remodeling your property, paying off debt, or paying for unforeseen needs.

Before you sign anything, it’s crucial to carefully read the terms and conditions of your home equity loan. Please feel free to contact a PenFed representative if you have any queries or worries concerning the loan.

Where are the PenFed Home Equity Loans available?

The qualifying members of PenFed Credit Union, a nationwide credit union, may apply for a PenFed home equity loan. Nevertheless, not all PenFed goods and services are offered everywhere. Alabama, Arizona, California, Colorado, Florida, Georgia, Hawaii, Maryland, North Carolina, Nebraska, New Jersey, New York, Oregon, Pennsylvania, Tennessee, Texas, Virginia, and Washington, D.C. are among the states where PenFed Credit Union has locations.

PenFed Credit Union provides online and mobile banking services in addition to its physical locations, which may be accessible to members all over the country. Visit their website or get in touch with them personally to see whether you qualify for membership and to learn more about PenFed Home Equity Loans and other offerings.

How to get connected with penfed customer service?

You can reach PenFed customer care by calling:

Go to the PenFed website and click the “Contact Us” tab at the top of the page to access it. You can then select the category of your inquiry and locate the proper contact details from there.

Contact PenFed customer care at 1-800-970-7766, available Monday to Friday from 9:00 AM to 9:00 PM EST, and on Saturday from 9:00 AM to 5:00 PM EST.

Utilize the live chat function to speak with a customer service agent during business hours by using the live chat feature on the PenFed website.

Visit a PenFed branch: You can go to one of the PenFed branch locations if you’d rather speak to a customer support agent in person. On the PenFed website, a list of branch locations can be found.

To ensure a quick and easy transaction, it’s crucial to have your account information prepared before calling PenFed customer support.

Pros and cons of PenFed Home Equity Loan

Pros

- Reduced interest rates: Compared to unsecured loans like credit cards and personal loans, PenFed home equity loans often have lower interest rates.

- Predictable payments: PenFed Home Equity Loans offer predictable payments with a fixed interest rate and monthly payments, which can make budgeting simpler.

- Access to funds: A home equity loan can give you access to a sizeable sum of money that you can use for a range of things, including home renovations, debt consolidation, or large expenditures.

- Possible tax advantages: A home equity loan’s interest payment may, in some circumstances, be tax deductible.

- Prepayment penalties are not charged with PenFed Home Equity Loans, so you can pay off your loan early without incurring any additional costs.

Cons

- The danger of foreclosure: Since your house backs home equity loans, you run the risk of losing it to foreclosure if you fall behind on your payments.

- PenFed Home Equity Loans may be subject to additional expenses, such as closing costs, title search fees, or fees for appraisals.

- Lengthier loan terms: Unsecured loans often offer shorter loan periods than home equity loans, which could result in you paying a higher interest rate over time.

- Equity requirement: You must have enough equity in your house to be eligible for a home equity loan, which may lower the amount you are able to borrow.

- Creditworthiness: PenFed Home Equity Loans have strict eligibility requirements, including a high credit score and a solid employment history.

Before determining whether a PenFed Home Equity Loan is the best financial option for your particular circumstances, it’s critical to consider the potential advantages and hazards of such a loan. Before requesting a home equity loan, take into account your financial objectives, capacity for payback, and general financial situation.

Must read- Best American Web Loan Reviews-Is AWL Best For You?

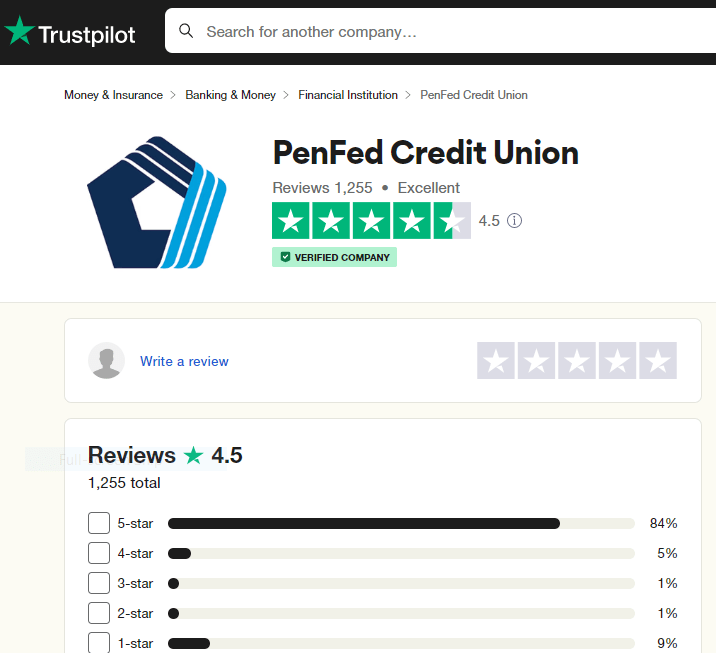

PenFed Home Equity Loan Reviews

There are great reviews about penfed credit union HELOC review on Trustpilot, and other third-party ratings and review websites. Penfed has more than 1,000 reviews with excellent ratings on Trustpilot. here, in the image below you can see. More than 80% of people have given 5-star reviews about penfed.

Conclusion of PenFed Home Equity Loan

In conclusion, homeowners who want to tap the equity in their house for significant expenses or debt consolidation may find a PenFed home equity loan to be a wonderful option. This kind of loan can offer substantial financial advantages due to its low-interest rates and accommodating repayment arrangements. The potential loss of your home should you default on the loan is just one of the hazards and requirements to be mindful of. Before deciding on a PenFed Home Equity Loan, it is essential to conduct due diligence, weigh your options, and speak with a financial expert.